How it pays for itself

No public capital, no public revenue subsidy, no public land transfer. The visitor rooms above pay for the public deck below.

Four concepts that would work

The site can support a range of viable schemes. Concept C — The Vessel — is recommended.

| Concept | Suites | Storeys | Total cost | Year 3 surplus | Risk |

|---|---|---|---|---|---|

| A · The Promenade | 0 | 2–2.5 | £8.8m | (modest) | Low |

| B · The Exchange | 5 | 3–3.5 | £13.2m | £260k | Low–med |

| C · The Vessel (recommended) | 10 | 4–4.5 | £18.0m | £670k | Medium |

| D · The Crown | 12 + 2 long-stay | 4.5 | £19.4m | £810k | Med–high |

Concept C — Year 3 mature operations

After debt service and maintenance

- Interest cover: ~£645k / year on senior debt

- Maintenance reserve: £240k / year (1.5% of replacement cost)

- Free cash for civic reinvestment: ~£428k / year

- Of which ~£248k flows to the Community Innovation Fund

Stress tests — Year 3

The model is tested against the worst credible scenarios. The project survives all of them.

| Scenario | Suite revenue | Total revenue | Result |

|---|---|---|---|

| Central case (£425, 65%) | £1,008k | £2,258k | Operating surplus £1.31m |

| Conservative (£350, 60%) | £767k | £2,016k | Operating surplus £1.07m |

| Stress (£290, 50%) | £529k | £1,779k | Operating surplus £834k — still covers debt |

| Upside Year 5 (£495, 70%) | £1,265k | £3,045k | Operating surplus £2.02m |

What the stress tests show

The project survives the worst credible scenario — £290 ADR at 50% occupancy — and still covers debt.

Below that level, the project is not commercially viable, and the team would not pretend otherwise.

The corporate retainer revenue (Section 9) is the key resilience layer. Without it, the project's risk profile rises sharply.

The blended six-layer funding stack

Total project cost £18.0m (Concept C). Funded through a six-layer blended stack at ~3.6% blended cost of capital.

| Layer | Share | Cost |

|---|---|---|

| Senior debt | 40% | 5.5–6.0% |

| Patient capital (HNW, family offices) | 25% | 3–4% |

| Foundation grants | 15% | 0% |

| Community shares | 7% | 2% |

| Civic Room-Night Bank | 5% | 0% (pre-paid) |

| Founder equity | 8% | 5% |

| TOTAL | 100% | ~3.6% blended |

Cost plan summary

| Element | Amount | % |

|---|---|---|

| Site purchase and acquisition | £2,246k | 12.4% |

| Surveys, planning, consents | £156k | 0.9% |

| Construction (£4,000/m²) | £10,600k | 58.4% |

| FF&E and fit-out | £700k | 3.9% |

| Specialist works and art | £418k | 2.3% |

| Professional fees | £1,406k | 7.7% |

| Finance during build | £450k | 2.5% |

| Pre-opening | £180k | 1.0% |

| Working capital reserve | £360k | 2.0% |

| Contingency | £1,640k | 9.0% |

| TOTAL | £18,156k | 100% |

The construction rate of £4,000/m² is benchmarked against the Guernsey 2022 baseline (~£3,200/m²) plus 12–15% construction inflation, plus 10–15% premium specification uplift, plus single-digit coastal complexity. It is at the lower end of the credible range.

Phase 0 deliverable: QS pre-tender estimate validating this rate against three named comparable Channel Islands projects of similar scale and specification.

Where the surplus goes — the affordability waterfall

The community feedback report was clear that affordability is not a marketing line — it is the precondition for public legitimacy. The surplus waterfall is sequenced to match.

| Priority | Allocation | Annual amount |

|---|---|---|

| 1 | Senior debt service | ~£645k |

| 2 | Maintenance reserve (1.5% of replacement cost) | £240k |

| 3 | Youth programme (Clause 3 — minimum, hard-coded) | £25k |

| 4 | Affordability programme — older-resident discounts (Clause 2), pay-it-forward coffee fund, swimmers' rates, family-rate menu | £35–55k |

| 5 | Patient capital coupon | ~£135k |

| 6 | Community Innovation Fund | ~£248k |

What this means in practice

If the project's commercial side struggles, the youth programme is preserved before café upgrades and before suite refurbishment. The affordability programme is preserved before discretionary spending. Senior debt and maintenance come first because the building must survive — but the public-benefit commitments are sequenced ahead of operator comfort.

This is the mechanism that prevents the project becoming "another expensive thing for a small number of people" if commercial pressure builds in years 6, 8, or 12.

Five-year revenue build

| Year | Stage | Revenue |

|---|---|---|

| 1 | Construction + soft launch | £0.45m |

| 2 | Building opens, suites at 50% | £1.55m |

| 3 | Full operations, suites at 65% | £2.26m |

| 4 | Mature, suites at 70% | £2.70m |

| 5 | Self-sustaining, suites at 75% | £3.05m |

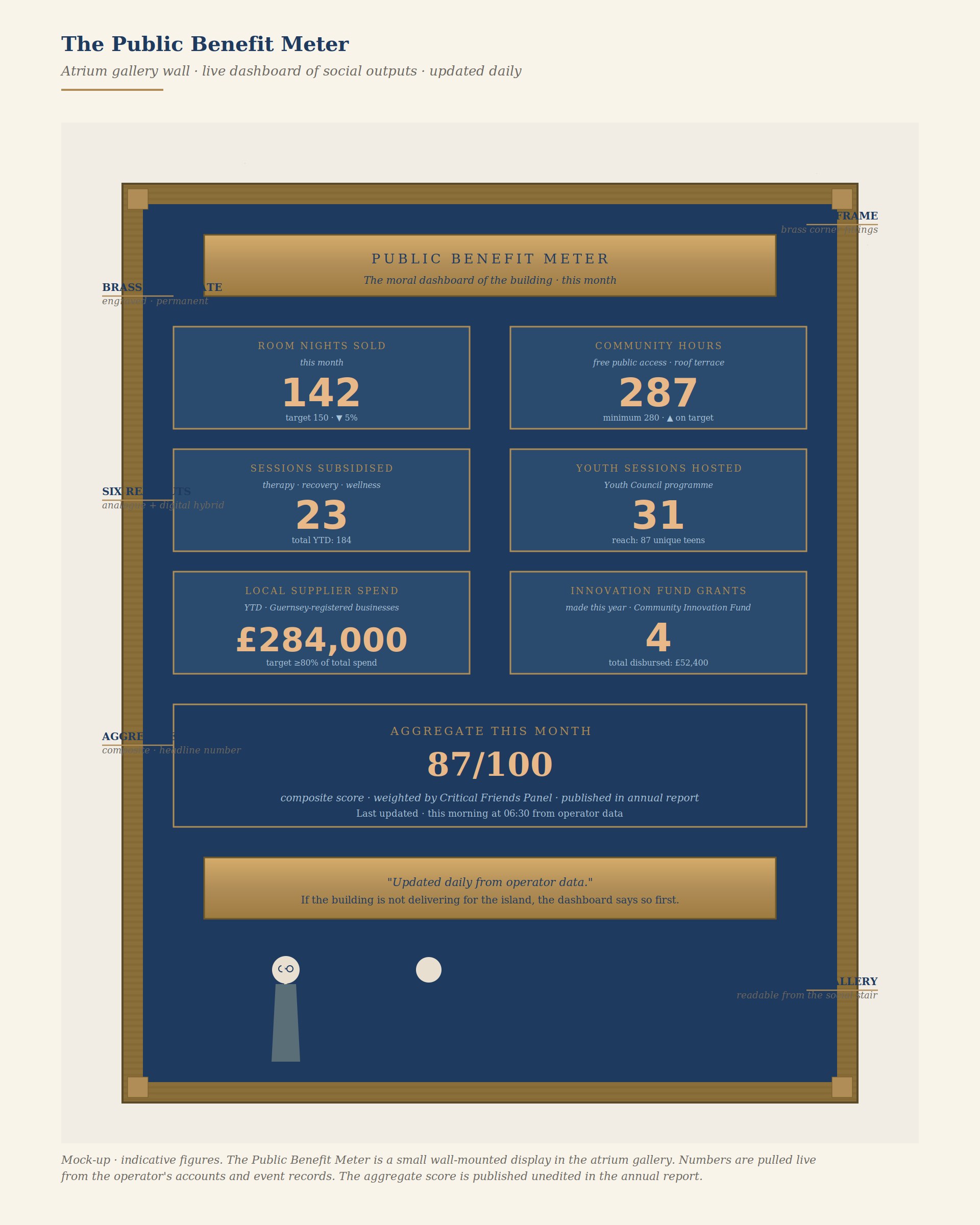

The Public Benefit Meter

A live wall-mounted dashboard in the atrium gallery. The numbers are pulled daily from the operator's accounts and event records. The aggregate score is published unedited in the annual report.